by Jeremy Bryan, CFA

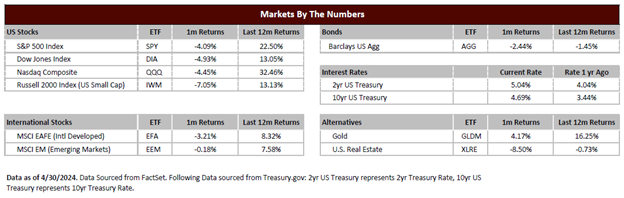

Markets faced their first real correction in 2024 as stocks declined for the month. One of the reasons for the correction was renewed inflation fears as recent data points were worse than expected.

There is no doubt that prices are rising, and US consumers are bearing a greater burden at the gas station and in the grocery store. We have seen a significant decline in the inflation rate since the peak in 2022, but this does not mean that prices are getting cheaper. A lower inflation rate only means that goods and services are getting more expensive at a slower rate.

The rate of inflation, and the resiliency of the US economy, has also given less credence to the notion that the US Federal Reserve will cut rates significantly in 2024. Already, expectations have been reduced from six or seven expected cuts in 2024 to a more rational one or two. Our view has been relatively consistent in this matter – the Fed will not preemptively move to cut rates until they have confidence that inflation is under control. The only actions that will spur the Fed to cut rates are either a) proof of normalized inflation or b) deteriorating economic conditions where cuts are needed to avoid a significant recession.

Our stance remains that there are no near-term signals that the US economy is headed into recession. We also believe that inflation is slowly progressing toward normalcy, but we have to acknowledge that it may take longer than originally thought. This would lead us to the conclusion that the Fed Funds rate may stay at the same levels throughout summer and potentially all of 2024.

Now, does this mean economic calamity and a massively declining stock market are ahead? No, it does not. Markets can move in the short term on Fed actions, but we believe business fundamentals still drive the long-term prices of stocks. As a result, corporate earnings growth is a much larger factor for us than Fed actions.

We are in the middle of “earnings season” right now when companies report their first quarter results and discuss current trends. The results thus far have been relatively positive. Companies are, more often than not, exceeding their expected results and offering outlooks that suggest continued growth in business activity.

This is not to say that there are no concerns, however. There are some indications that consumers are starting to adjust spending patterns based on persistently high prices. While housing activity has been the front and center of higher costs affecting activity, there are now indications that spending in restaurants is slowing as well. Consumer spending is the most significant driver for the US economy, so we watch very closely for any changes to spending patterns. While it is too early to say definitively that consumers are pulling back spending as a result of high prices, there are more mixed signals now than in past quarters.

For bonds, the headwind of rising rates has once again led to a difficult start to the year. As a reminder, 2023 also showed negative performance for bonds all the way until September before rebounding aggressively in the fourth quarter. We believe bond yields are currently at relatively opportunistic levels. If inflation is progressing in the right direction, and our opinion that the Fed is done raising rates (and may actually begin to decrease) proves correct, then bond investors would have both high current income and the potential for price return if interest rates were to fall.

Given the prices of both stocks and bonds, we believe a prudent action is to have a blend of both safe and growth assets. Having investments that protect from severe declines, but having other assets that participate in rallies, is entirely possible. Having a safety net provides some protection in case bad times occur. Second, because of higher interest rates, the yield from relatively safe instruments is higher now than it has been in recent years. For savers, this is a benefit as it does not require a large sacrifice of return to have a portion of safe assets in the portfolio.

On the other side, setting up a safety net does not mean being in all cash until investors are given an “all clear” signal from the markets. Understand that risks are always present in the markets and concerns never really go away, but they just pivot from one to another. As a result, investing in stocks can be a bumpy ride, but history tells us that pitfalls tend to be short lived, and the times of prosperity can last far longer than most expect. Therefore, a prudent allocation that blends both safe and growth assets that fit your investment objectives and risk tolerance remains the best way to achieve your long-term financial goals.

This endorsement of Gradient Investments, LLC is provided by an investment advisor who refers clients to Gradient Investments, LLC. A conflict of interest exists because this investment advisor receives a portion of the annual management fee charged by Gradient Investments, LLC, based on the assets under management of this investment advisor’s clients. This endorsement could assist in the investment advisor increasing the assets placed with Gradient Investments, LLC, and therefore their compensation. These investment advisors are not affiliated with or supervised by Gradient Investments, LLC.